Financial education is the knowledge that helps you effectively manage your money. It’s not just about theoretical concepts of the financial market; it’s also about learning how to apply this information in practice.

With financial education, you can use financial products and services that align with your needs and resources, all to increase your personal well-being. Being financially literate doesn’t mean you have to be a specialist or an expert.

Your relationship with your finances

The way you manage your money daily, as well as the decisions you make for the future, can influence both your short-term financial security and your long-term stability.

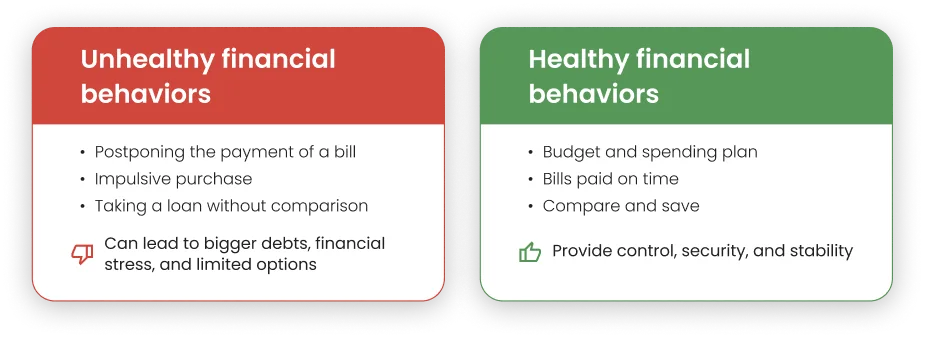

Perhaps you’ve put off paying a bill, made an impulsive purchase, or chose a loan simply because it seemed like the quickest solution without comparing other offers. While these behaviors may seem small or insignificant at the time, they can lead to greater debt, financial stress, and even limit your options when you need resources.

On the other hand, healthy financial behavior, a result of financial education, means planning for your spending, paying your bills on time, analyzing financial products before deciding, and setting aside money for your goals. These actions give you control over your budget, reduce your risks, and increase your chances of achieving personal objectives, whether it’s saving, investing, or simply having the peace of mind that comes with being prepared for the unexpected.

Saving Methods

Saving isn’t just about putting money aside when you “have some left at the end of the month.” It’s a strategy that helps you organize your budget to achieve financial security, reduce stress, and meet your personal goals.

The 50/30/20 Rule

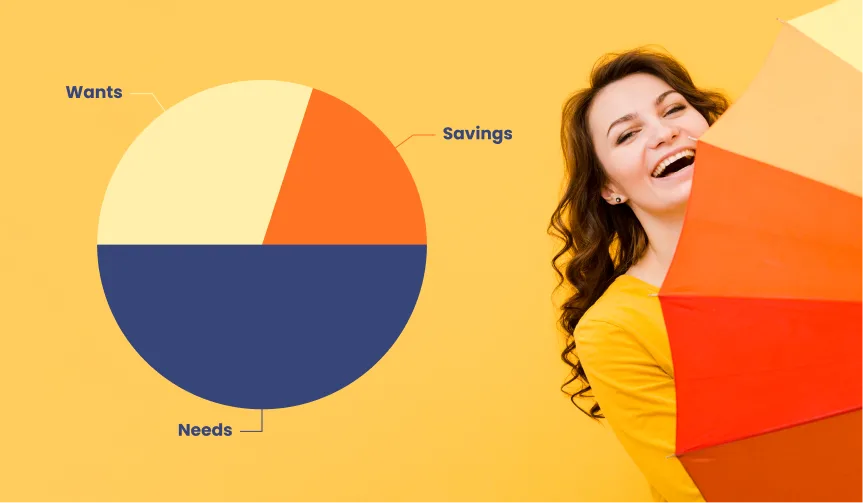

This rule is a simple way to divide your monthly income:

- 50% for Needs: This covers essential expenses like rent/mortgage, utilities, food, transportation, and bills, everything that’s mandatory.

- 30% for Wants: This includes things that please you but aren’t essential, such as dining out, vacations, hobbies, and subscriptions.

- 20% for Savings and Investments: This is money set aside for future goals: an emergency fund, a down payment on a house, or retirement investments.

The advantage of this rule is that it provides a clear framework and a balance between the present (enjoying your life) and the future (being prepared). The rule itself is a practical financial education tool that helps you manage your resources more efficiently.

The Emergency Fund

One of your first financial goals should be to create an emergency fund. This is a sum of money set aside for unforeseen situations, such as job loss, health problems, or urgent home or car repairs.

How much should you have? Experts recommend saving between three and six months’ worth of essential expenses.

Where should you keep it? In a separate, accessible account, but not on your everyday debit card, to avoid the temptation of using it for other things.

Why is it important? It gives you peace of mind and security. Instead of borrowing money or going into debt, you have the necessary resources to get through difficult periods.

The difference between good debt and bad debt

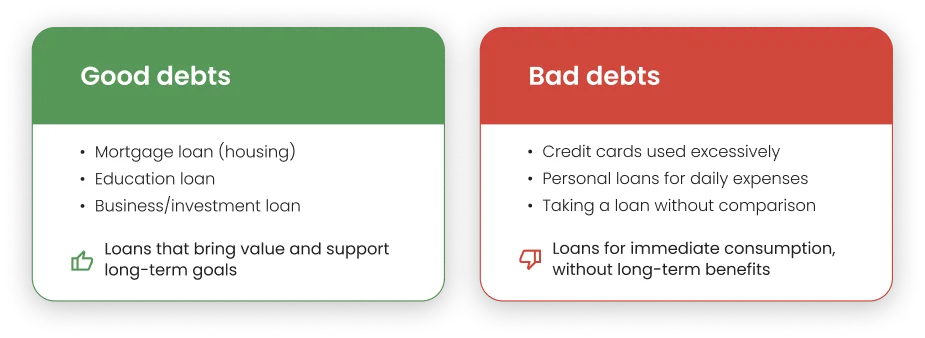

A key aspect of personal financial education is understanding that good debt helps you build value over time, while bad debt erodes your income without leaving anything behind.

Good debt

These are loans that help increase your financial value over time or achieve important long-term goals. Essentially, the money you borrow “works” for you.

Examples:

- A mortgage for a home (it helps you become a homeowner, and over time, you pay for something that becomes yours).

- A student loan (investing in knowledge and skills can increase your future income).

- A business or investment loan (if it generates a return greater than the cost of the interest).

Characteristics:

- They have the potential to bring long-term value.

- They are carefully planned and taken on with consideration.

- The interest rates and conditions are sustainable in relation to your income.

Bad Debt

These are loans that don’t bring future value and, most of the time, consume your monthly budget without leaving anything in return.

Examples:

- Consumer loans for impulsive purchases (a new phone, an expensive vacation).

- Excessive use of a credit card for daily expenses.

- High-interest loans like “payday loans.”

Characteristics:

- They are for momentary wants, not real needs.

- They reduce your ability to save and increase the risk of over-indebtedness.

- The costs (interest, fees) exceed the benefit you gained from the purchased product.

Insurance as a financial protection tool

Since ancient times, long before the concept of financial education existed, people felt the need to protect their goods, merchandise, valuables, and even their own lives. The first forms of insurance emerged with the development of maritime trade during the time of the Code of Hammurabi.

From then until now, the principle has remained the same: insurance protects against the financial consequences of unforeseen risks.

An unexpected event can lead to significant losses: repairing or replacing belongings, high medical costs, or other urgent expenses. In such situations, insurance can make a big difference, helping you manage the financial impact more easily. Alternatively, you could use your savings, which should maintain their value over time by offsetting the effects of inflation.

While we can’t eliminate risks, we can take action to prevent them. And if a risk does materialize, it’s important to reduce its effects as much as possible. That’s why it’s useful to learn about the available financial products that can offer you an extra layer of protection.